Key topics:

-

AI mega-IPOs may weaken broader stock market momentum

-

Rising equity supply could end years of “de-equitisation”

-

Tech rally faces risks from liquidity drains and insider selling

Sign up for your early morning brew of the BizNews Insider to keep you up to speed with the content that matters. The newsletter will land in your inbox at 5:30am weekdays. Register here.

Support South Africa’s bastion of independent journalism, offering balanced insights on investments, business, and the political economy, by joining BizNews Premium. Register here.

If you prefer WhatsApp for updates, sign up to the BizNews channel here.

By Tej Parikh

A potential deluge of AI-related equity supply removes a source of upthrust for prices

This article is an on-site version of the Free Lunch newsletter. Premium subscribers can sign up here to get the newsletter delivered every Thursday and Sunday. Standard subscribers can upgrade to Premium here, or explore all FT newsletters

The prospect of blockbuster listings from SpaceX, Anthropic and OpenAI has excited stockpickers. The S&P 500’s AI-driven growth has thus far been underpinned by chipmakers and hyperscalers. These initial public offerings would give investors direct exposure to model developers (and a rocket company).

But history suggests the issuance buzz may in fact mark the beginning of the end of the tech rally.

Read more:

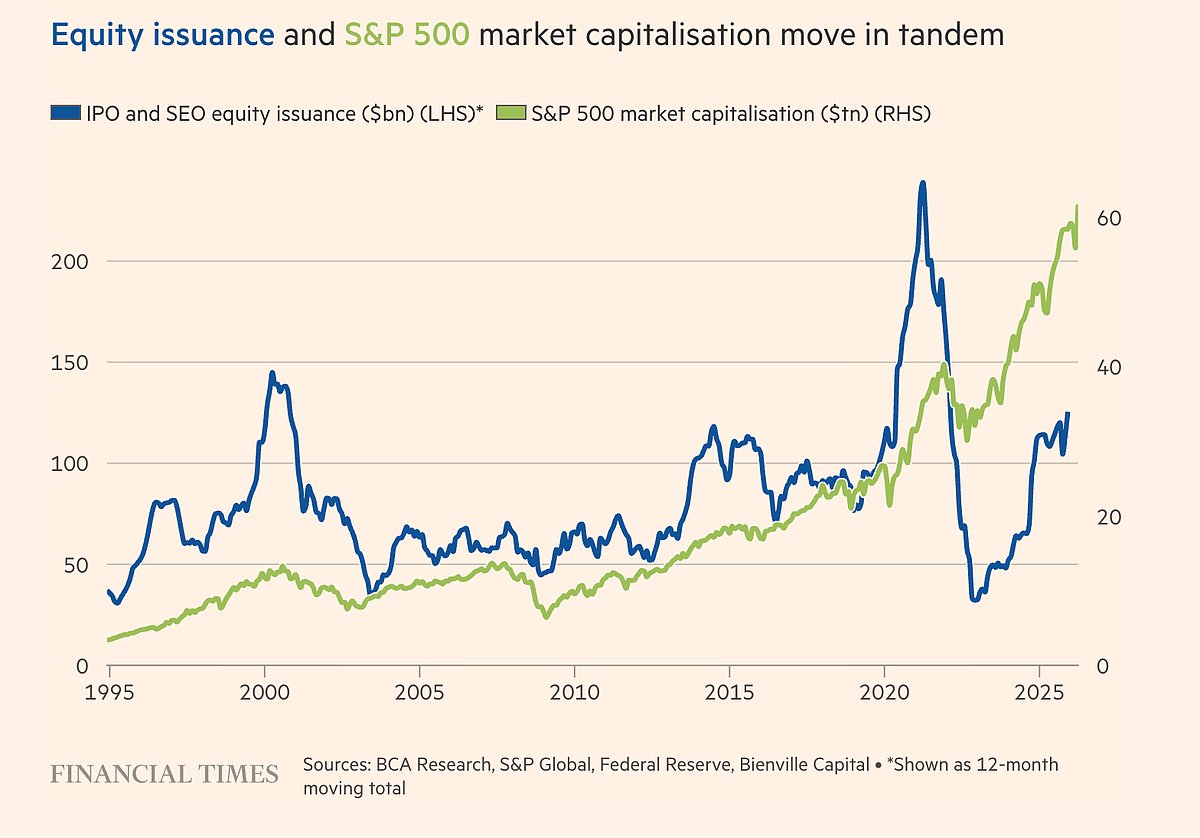

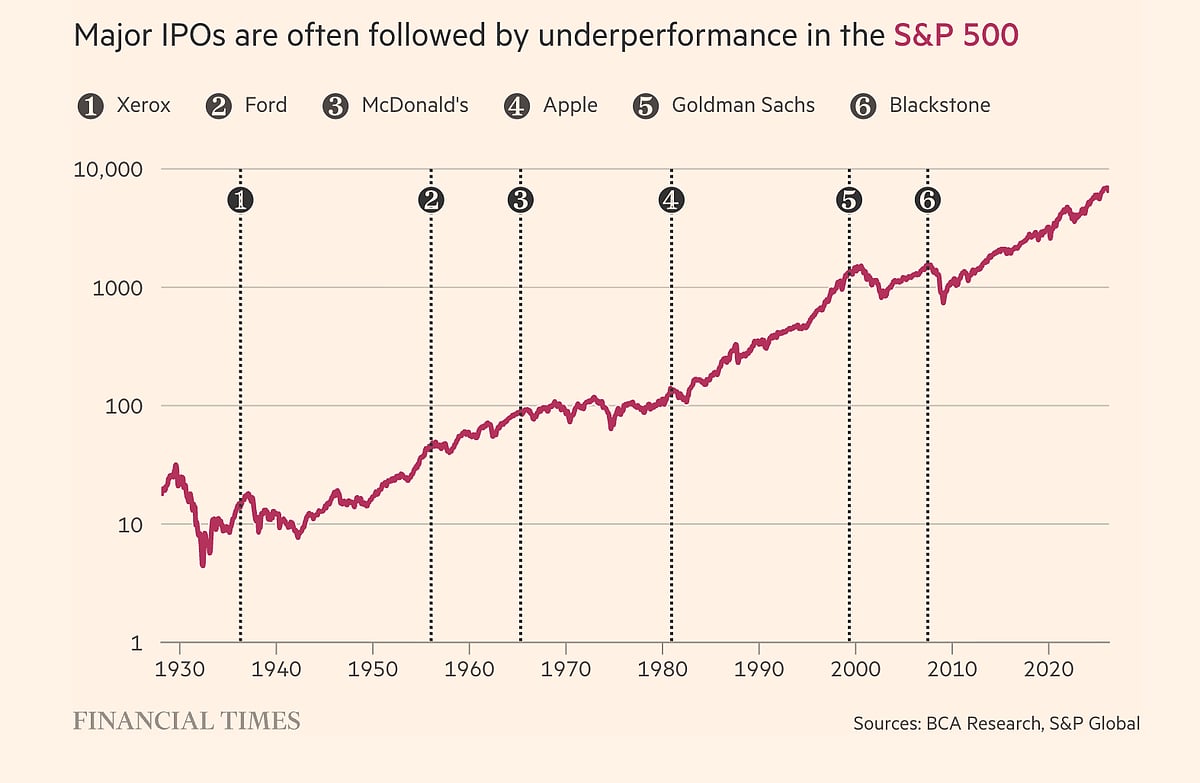

Long-run data collated by BCA Research shows that the S&P 500 tends to underperform after major IPOs. This is partly because an increase in the supply of stocks absorbs capital near market highs and leaves fewer funds available to sustain the broader market.

Right now, analysts are confident that the market can absorb new issuance. But the three aforementioned companies could have a potential collective valuation of around $4tn, which would amount to about 6 per cent of the US public equity market. That’s on par with equity expansions during the late-1990s dotcom bubble. For measure, the cumulative market value of all US IPOs at first close between 1980 and 2025 was about $12.5tn on an inflation-adjusted basis.

The new issuance comes as equity supply could rise more broadly, perhaps compounded by other IPO candidates such as tech companies Stripe and Databricks.

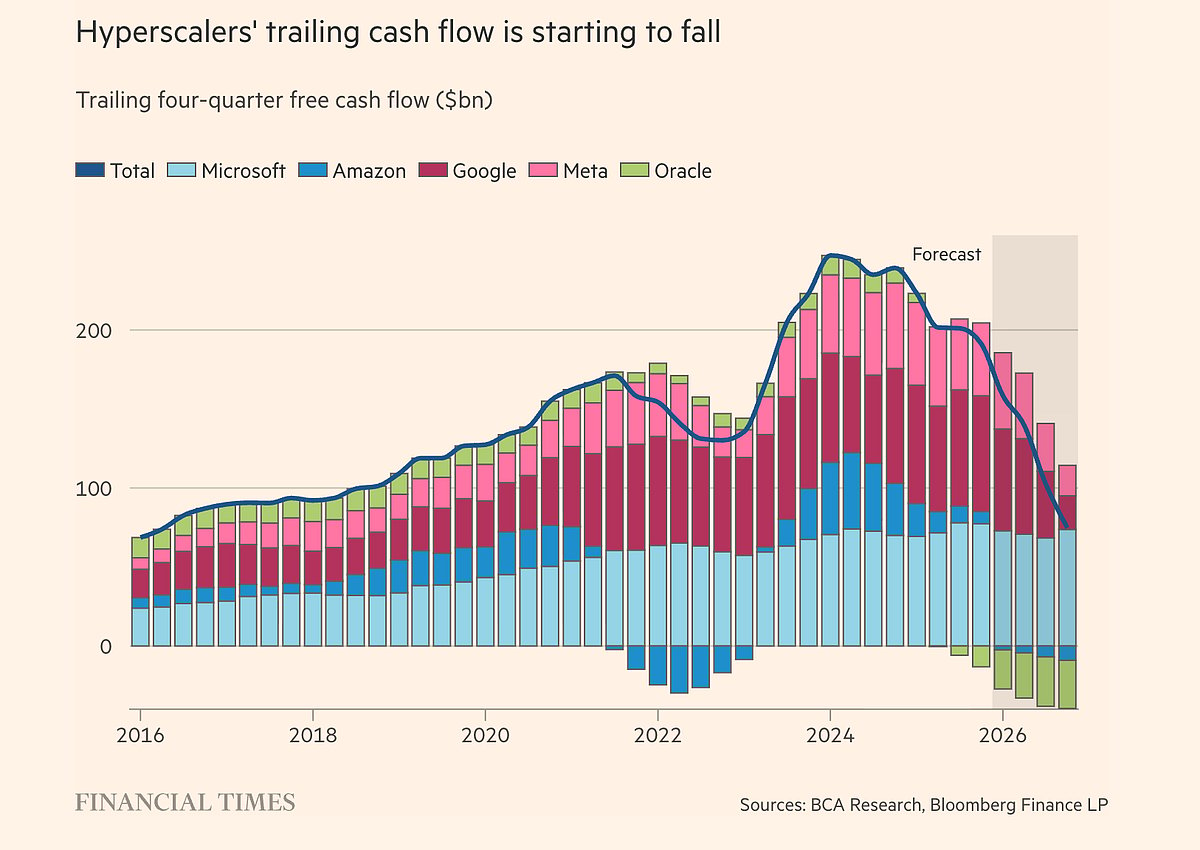

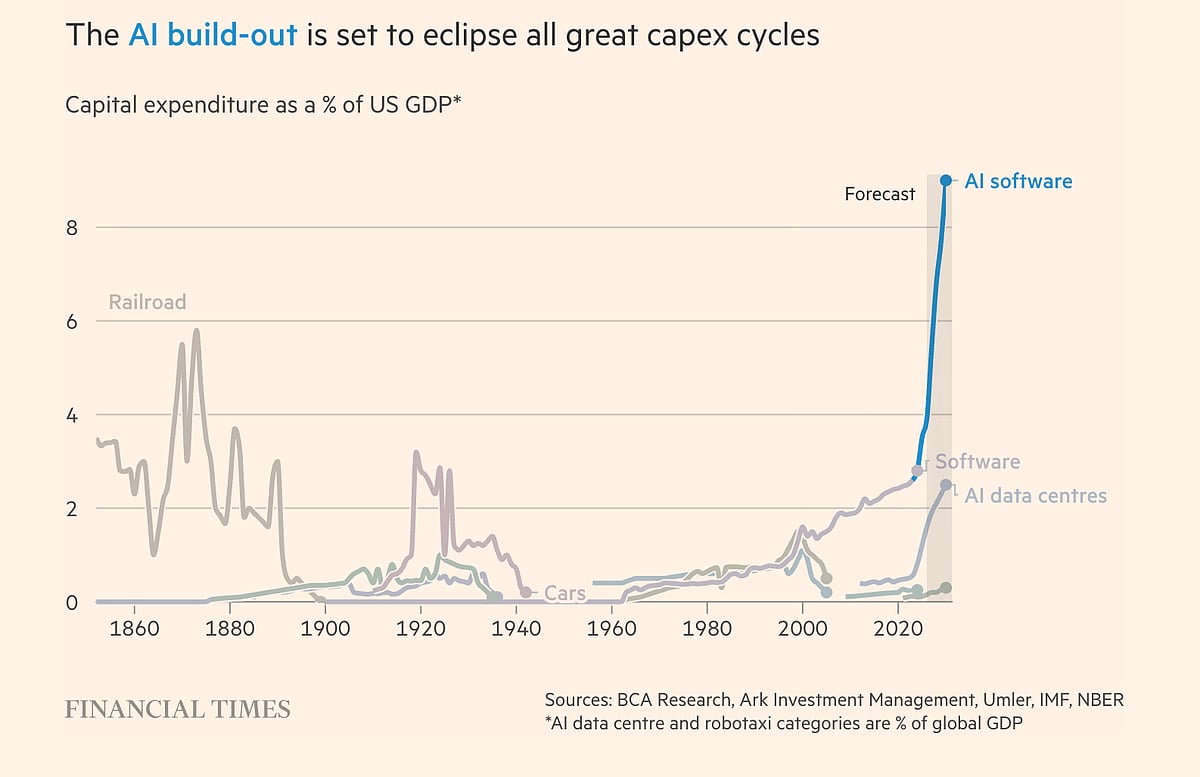

US hyperscalers’ capital expenditure as a share of GDP is set to far surpass the 19th-century railroad build-out. Until now, their spending has largely been funded through operating cash flow. But as this has waned, some Big Tech groups have reduced their stock buybacks and used debt to finance expenditure. They could also issue new shares to finance further investment or buy other companies.

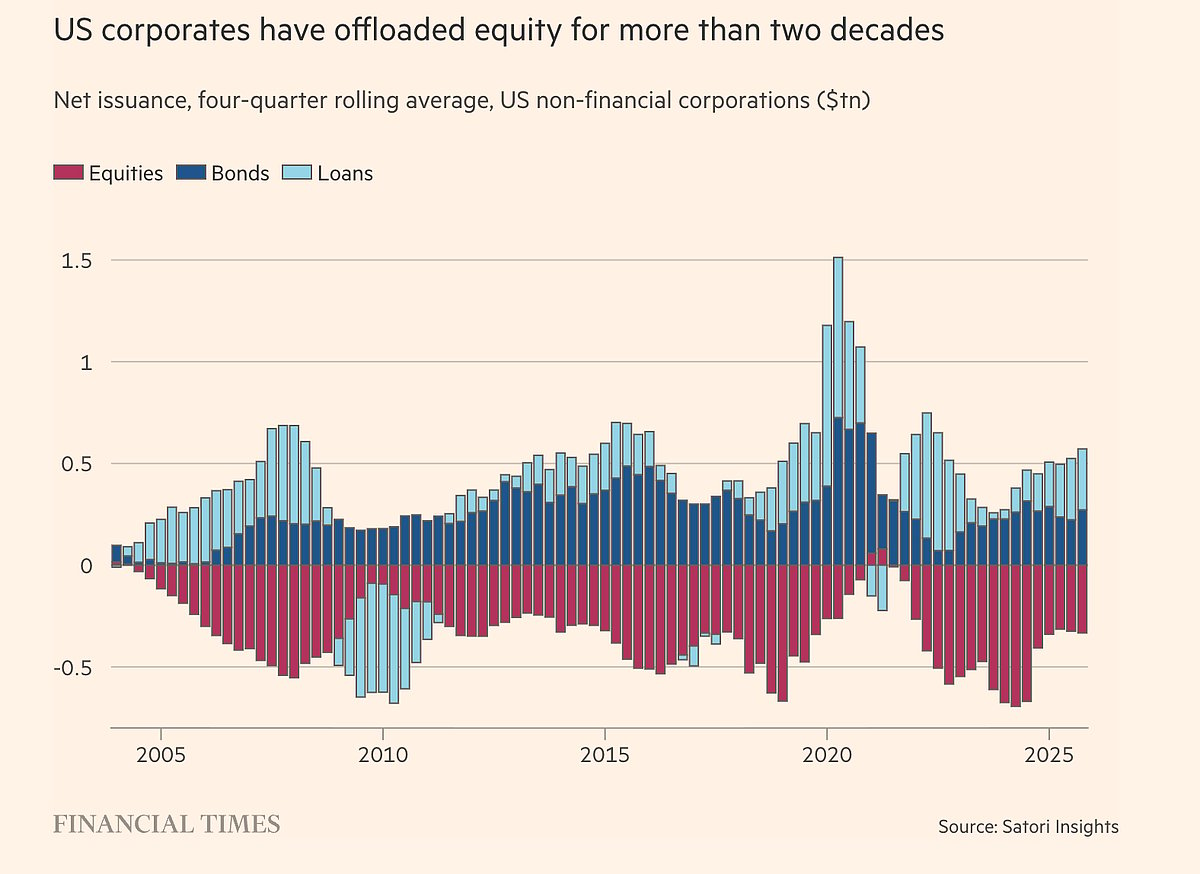

A rising supply of stocks would mark a structural shift. Equities have fallen in supply over the past two decades as a result of delisting, share buybacks, mergers and acquisitions activity and the growth of private markets.

The US equity base — that is, market capitalisation divided by price — is now around 7 per cent below its mid-2000s level. The number of US-listed companies has more than halved since 1995. Meanwhile, liquidity from quantitative easing following the 2008 financial crisis and the Covid-19 pandemic has helped prop up demand for equities.

This era of “de-equitisation” provided an uplift to the stock market, notes Robert Buckland, former chief global equity strategist at Citigroup. “A shrinking supply of public equities coupled with high demand is a key reason why the market has kept rising in the face of rising interest rates, trade wars and geopolitical volatility,” he says.

But as Buckland recently noted in an FT opinion piece, this supply “put” may now be coming to an end. “Equitisation plays a part in killing off every bull market. We haven’t seen that yet, but these IPOs may be the beginnings,” he told me. New Federal Reserve chair Kevin Warsh’s aim to reduce the size of the US central bank’s balance sheet may also drain liquidity (as might rising interest rates).

Though high equity supply creates absorption challenges for the market, there are many reasons why stocks might appear to be weaker after strong issuance. “It’s not necessarily causal. IPO booms tend to come with strong markets and hype. IPOs, equity-funded acquisitions and private equity queuing up to sell are all symptoms of an expensive market and signs that insiders want out,” notes Matt King, founder of Satori Insights.

Indeed, what happens after the typical six-month lock-up period post-IPO, when insiders gain the ability to sell, will be indicative.

Read more:

Many have called the top of the tech rally before, yet the market has continued to climb in the face of unprecedented shocks. Several factors could support upwards momentum for the S&P 500: advancements in AI, index reweighting, shifting capital allocations as new issuance arrives and investment of existing cash piles.

Even so, if the mega IPOs materialise — and greater AI-related equity supply follows — the market could lose some of the upthrust investors have, until now, taken for granted.

© 2026 The Financial Times Ltd.

Sign up for your early morning brew of the BizNews Insider to keep you up to speed with the content that matters. The newsletter will land in your inbox every morning on weekdays. Register here.

Support South Africa’s bastion of independent journalism, offering balanced insights on investments, business, and the political economy, by joining BizNews Premium. Register here.

If you prefer WhatsApp for updates, sign up to the BizNews channel here.